The chemistry of clean laundry, the economics most consumers never calculate, and why India's ₹55,000 crore fabric care market is quietly splitting into two countries

There's a simple experiment you can run tonight.

Take two identical white cotton shirts. Wash one with your regular powder detergent. Wash the other with a liquid detergent of the same brand. Dry both the same way. Now hold them up to sunlight and compare.

The liquid-washed shirt will be marginally whiter. Not because liquid detergent has better marketing - but because powder detergent, by the laws of chemistry, cannot fully dissolve in the water temperatures most Indian households actually use. Those undissolved granules leave a faint mineral residue in the fabric weave that accumulates over dozens of wash cycles, gradually greying white clothes from the inside out.

This isn't an opinion. It's dissolution kinetics. And it's the real reason India's fabric care market is undergoing a structural shift that most consumers don't fully understand.

What Actually Happens Inside Your Washing Machine

Before discussing markets, it's worth understanding what cleaning actually is - at the molecular level.

A "stain" is simply a foreign molecule that has bonded to textile fibers. Turmeric is a polyphenol (curcumin) that binds through hydrogen bonds. Blood is a protein (hemoglobin) that cross-links with cotton cellulose. Cooking oil is a triglyceride that embeds itself in hydrophobic pockets between fibers.

Think of it this way: a stain isn't sitting on your shirt - it's chemically gripping the fabric, like a vine wrapping around a fence. Different stains grip differently, and each type of grip requires a different tool to pry it loose.

Surfactants are the primary weapon. These are molecules with a split personality: one end is hydrophilic (loves water), the other is hydrophobic (loves oil). In solution, surfactants arrange themselves into structures called micelles - tiny spheres where the hydrophobic tails point inward, creating an oil-trapping cavity, while the hydrophilic heads face the water. When a micelle encounters a grease stain, the hydrophobic tails pull the oil molecule away from the fabric and trap it inside the sphere. The hydrophilic shell then keeps the whole package suspended in water, preventing re-deposition.

Imagine a tiny soccer ball made of thousands of molecules. The inside of the ball is oily; the outside is watery. The ball rolls over a grease stain, swallows it into its oily core, and floats away in the wash water - carrying the stain with it. That's a micelle. That's what your detergent actually does. Millions of these microscopic soccer balls, doing this millions of times per wash cycle.

This mechanism works identically in powders and liquids. The difference is in the supporting cast.

Builders (sodium tripolyphosphate, zeolites) soften water by sequestering calcium and magnesium ions - the minerals that make water "hard." Hard water ions react with anionic surfactants to form insoluble calcium stearate: soap scum. This is why the same detergent that produces rich lather in Bangalore (soft water, ~80 ppm hardness) barely foams in Jodhpur (hard water, 400+ ppm). Builders prevent this by grabbing calcium ions before they can neutralize surfactants.

In plain terms: hard water "kills" your detergent before it can do its job. Builders are the bodyguards - they intercept the minerals in water so the surfactants can focus on cleaning instead of fighting the water itself.

Enzymes are precision tools-biological scissors designed to cut specific stains like blood or oil. They are powerful, but they are also proteins that denature (break apart) in hot water and add significant cost.

This leads to a simple truth: enzymes are not required for every wash. For the 90% of daily laundry loads-light dust, sweat, and general freshening-surfactant action alone is sufficient.

This is why "Daily Wash" liquids (like Vow) exist. They strip out the expensive biological additives to focus purely on the core benefit of the liquid format: perfect dissolution and zero residue. It's smart engineering-paying for the chemistry you actually need for daily wear, not the chemistry required for a chef's apron.

The Dissolution Problem

Now consider what happens when you add detergent to water.

A liquid detergent is, by definition, already in solution. The moment it contacts wash water, surfactants and builders begin working immediately. There is no intermediate step.

A powder detergent must first dissolve. This requires three things: water temperature, agitation, and time. In laboratory conditions (40°C water, vigorous stirring), high-quality powders dissolve in 2–3 minutes. In real Indian conditions - 25°C tap water in winter, a semi-automatic machine with modest agitation - dissolution can take 8–12 minutes. Some fraction of the powder never dissolves at all.

This matters because undissolved detergent is worse than useless. Those white granules you occasionally find clinging to dark clothes aren't just aesthetically unpleasant - they're concentrated alkali deposits (sodium carbonate, sodium sulfate) that weaken fiber structure over time. Powder detergents typically maintain pH 10–11 in solution, but undissolved granules can reach localized pH of 12+. At that alkalinity, cotton cellulose chains begin to hydrolyze. Fabric literally weakens from the inside.

Here's an analogy: imagine dissolving sugar in cold water versus hot chai. In hot chai, the sugar vanishes instantly. In cold water, half of it sits at the bottom of the glass no matter how hard you stir. Now imagine that undissolved sugar was mildly corrosive. That's what undissolved powder detergent does to your clothes - sitting in concentrated clumps against the fabric, slowly eating into it, wash after wash.

Liquid detergents, by avoiding this dissolution step entirely, eliminate the problem. They also allow more precise dosing - a measured capful versus an approximate scoop - which reduces both overdosing (residue, fabric damage) and underdosing (poor cleaning).

This is the unsexy, chemistry-level reason that liquid detergents produce better outcomes. Not marketing. Not premiumization theatre. Just dissolution kinetics and pH control.

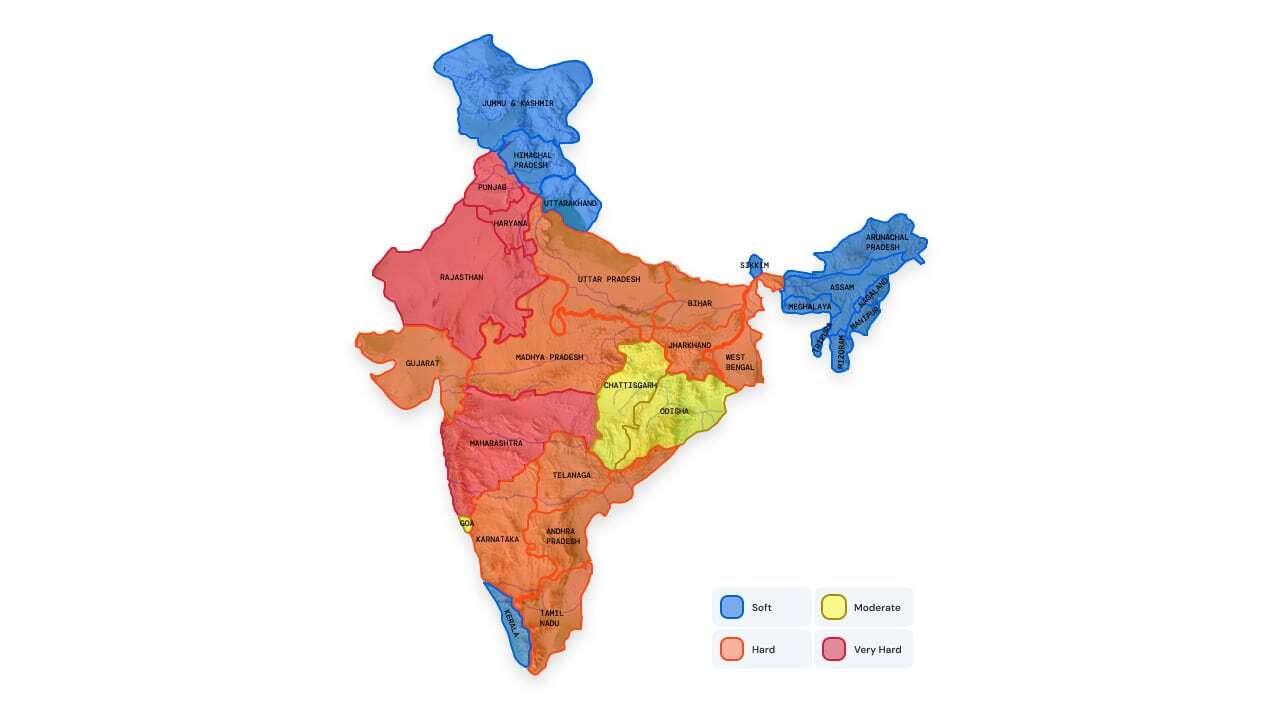

The Two Indias of Water Hardness

India's groundwater hardness varies enormously - from 50 ppm (essentially rain-soft) in the Western Ghats to 1,500+ ppm in parts of Rajasthan and Gujarat. The Central Ground Water Board monitors this through ~15,500 observation wells annually. The map of hardness looks nothing like the map of income or urbanization.

| Water Type | Typical Hardness (ppm) | Detergent Implication |

|---|---|---|

| Soft | 50–120 | powders dissolve adequately; both formats perform well |

| Moderate | 150–300 | liquids show measurable advantage in lather and cleaning |

| Hard | 200–450 | powder performance degrades; builder demand increases |

| Very hard | 300–1,500+ | powders severely impaired; liquid + supplementary softener often needed |

This geography creates a counterintuitive pattern: the regions where liquid detergent is most needed (hard water zones) are often the regions where it's least adopted - because these tend to be lower-income, less-urbanized areas where powder and bar formats still dominate on price.

Conversely, Cities which have softer water and theoretically less need for liquids - show the highest liquid penetration (reportedly 60%+ in urban pockets). The adoption there is driven by washing machine penetration and convenience, not water chemistry.

The opportunity, then, is in the mismatch: consumers in Rajasthan, Gujarat, and coastal Tamil Nadu would see the largest performance improvement from switching to liquid, but they're the last to switch because the per-unit price signals "premium."

The Per-Wash Economics Nobody Calculates

This is where things get interesting - and where consumers are systematically misled by pack-price comparisons.

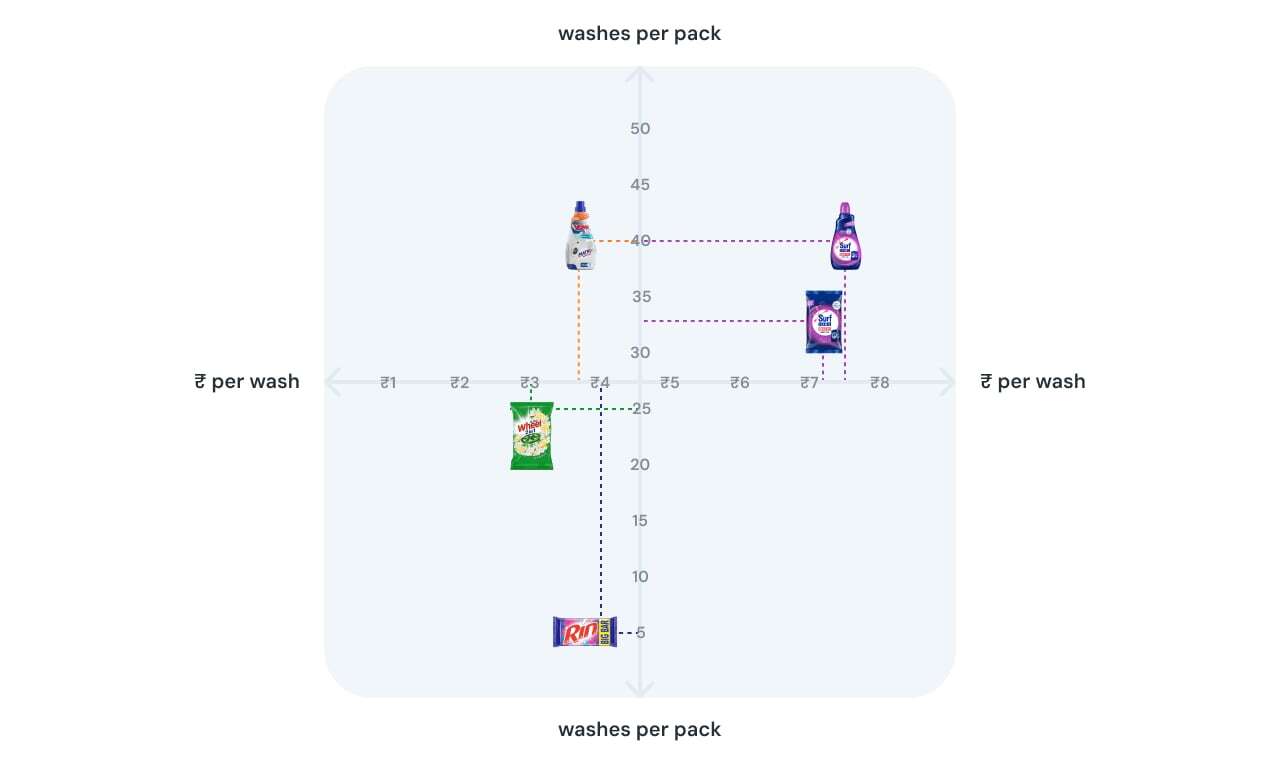

Let's do the maths. A typical Indian wash load is 2–3 kg of clothes.

| Format | Typical Product | Pack Price | Dose/Wash | Cost/Wash | Washes/Pack |

|---|---|---|---|---|---|

| Bar | Rin Bar 250g | ₹20 | ~50g | ₹4.0 | 5 |

| Powder (mass) | Wheel Active 1kg | ₹72 | ~40g | ₹2.9 | 25 |

| Powder (premium) | Surf Excel Matic TL 1kg | ₹240 | ~30g | ₹7.2 | 33 |

| Liquid (mid-tier) | Surf Excel Matic Liquid 1L | ₹299 | ~25ml | ₹7.5 | 40 |

| Liquid (value) | Vow Liquid Detergent 1L | ₹149 | ~25ml | ₹3.7 | 40 |

Three observations:

First - and this genuinely surprises most people - detergent bars are not the cheapest format per wash. A Rin bar costs ₹20, looks affordable, and feels like the budget option. But at ~50g per hand-wash load, you get just 5 washes from that pack. That's ₹4.0 per wash. Mass-market powder (Wheel at ₹72/kg) delivers 25 washes at ₹2.9 each. The "cheap" bar is actually 38% more expensive per wash than the powder sitting next to it on the shelf. Consumers perceive the opposite because they compare pack prices (₹20 vs ₹72), not cost-per-wash (₹4.0 vs ₹2.9). This is a fundamental information asymmetry in the market - and it runs even deeper at the liquid end, where people compare ₹72/kg to ₹299/litre without realizing the liquid yields 40 washes while the powder yields 25.

Second, the powder-to-liquid jump at the premium tier is negligible. Surf Excel Matic Powder at ₹7.2/ wash versus Surf Excel Matic Liquid at ₹7.5/wash - a 4% difference. Consumers perceive a massive gap because they see ₹240 versus ₹299 on the shelf. But per wash, they're virtually identical. The "premium" of liquid is an optical illusion created by pack-price comparison.

Third, the value private-label tier changes the equation entirely. Vow Liquid Detergent at ₹149/litre yielding 40 washes delivers a cost-per-wash of ₹3.7 - significantly cheaper than even mid-tier powders. This is the price point where liquid detergent becomes accessible to mass-market households that currently buy budget powders or even bars.

This is why private-label liquid detergent is one of the most interesting spaces in Indian FMCG right now. It's not about competing with branded liquids on marketing. It's about offering the format shift at a price that makes the per-wash economics comparable to - or better than - what consumers already pay for premium powders.

The Washing Machine Multiplier

India's washing machine penetration is roughly 18–20% of all households nationally. In urban India, it's closer to 40–45%. By 2030, with units growing at 11% CAGR and the market expected to reach 16+ million units annually, this number will approach 55–60% urban penetration.

Why this matters: washing machines don't just increase liquid detergent demand - they make powders actively problematic.

Semi-automatic top-loaders (still ~50% of India's machine park) have a dedicated wash tub where powder is added directly to water with clothes. Dissolution is imperfect. Residue accumulates in the tub, requiring periodic cleaning.

Fully automatic machines (growing rapidly, especially front-loaders) have dispenser drawers where detergent must flow through narrow channels to reach the drum. Clumped or slow-dissolving powder can block these channels, leading to uneven distribution. Manufacturers recommend liquid detergent in dispenser trays for this reason - not as a preference, but as an engineering requirement.

Front-loading machines, which use 40–50% less water than top-loaders, compound the issue. Less water means higher detergent concentration in the wash solution. Powder overdosing in a front-loader creates excessive suds that overwhelm the machine's limited water volume, triggering error codes and potentially damaging seals. (If you've ever seen your front-loader flash an error mid-cycle and wondered why - excess powder suds are among the most common culprits.) Liquid's precise dosing solves this.

The growth trajectory is clear: as washing machine penetration rises and the mix shifts from semi-automatic to fully automatic (and particularly to front-loaders), liquid detergent transitions from "nice to have" to "functionally necessary."

What the Market Numbers Actually Say

India's overall fabric care market is estimated at ₹55,000–60,000 crore annually, making it the single largest FMCG category. Within this:

-

Bars still account for roughly 35–40% of value (dominant in rural and lower-income segments)

-

Powders account for approximately 45–50% (the mass middle)

-

Liquids account for roughly 10% of value - but are growing at 4x the rate of the overall category

That 10% number is the headline. But it obscures a structural reality: in urban modern trade channels, liquids already represent 20–25% of fabric care sales. In quick-commerce, the share is even higher - possibly 30–35% - because the format attracts urban, machine-owning households that disproportionately use liquids.

Surf Excel alone crossed ₹10,000 crore in FY25 revenue, with its liquid portfolio delivering double-digit growth while the powder portfolio grew mid-single digits. The largest brand in India's largest FMCG category is seeing its growth engine shift decisively toward liquid.

At the national level, liquid penetration in Indian laundry care remains a fraction of developed markets (US: ~75%, EU: ~60%, Japan: ~90%). Even within Asia, countries at similar GDP-per-capita levels show higher liquid adoption. The structural runway is enormous.

What This Means for a Supermarket Shelf

For a retailer, the powder-to-liquid transition creates a specific challenge: the same consumer spending shifts from a low-margin, high-volume category to a higher-margin, lower-volume one.

Consider the shelf economics (based on actual modern trade margin data for the In-Wash category):

| Metric | Detergent Bar | Powder (Bucket Wash) | Matic Powder | Liquid Detergent | Matic Liquid |

|---|---|---|---|---|---|

| Sale share (offline) | 8.8% | 27.3% | 11.2% | 9.8% | 42.7% |

| Trade margin (TCI%) | 10.2% | 15.1% | 20.6% | 22.8% | 32.5% |

The pattern is striking: margins increase almost linearly as you move from bars to powders to liquids. Matic liquid - the fastest-growing sub-segment - delivers 32.5% trade margin, more than triple the bar segment's 10.2%. And it already commands the largest share of offline In-Wash sales at 42.7%.

This isn't a coincidence. Premium formats carry premium margins. But the compounding effect is what matters for retailers: matic liquid delivers both the highest margin and the highest sale share. Every percentage point of shelf space reallocated from bars or bucket-wash powder toward matic liquid generates disproportionate margin improvement.

There's a nuance, though: the consumer hasn't fully made the switch. Cut powder space too aggressively and you lose the customer who buys both - powder for regular loads, liquid for delicates or machine cycles. The transition period demands carrying both formats efficiently, which means the total laundry section must be intelligently merchandised rather than simply resized.

The Private-Label Opportunity

India's branded liquid detergent market is dominated by three players who collectively hold ~75% share. Their pricing reflects brand premium, advertising recovery, and distribution margin - not manufacturing complexity.

The actual manufacturing cost of liquid detergent is straightforward. It's a water-based formulation: 15–25% anionic surfactants, 5–10% nonionic surfactants, 2–5% builders, enzymes, fragrance, preservatives, and colourants. The raw materials for a litre of mid-tier liquid detergent cost ₹35-45. Packaging adds ₹15–25. Contract manufacturing and filling adds ₹10–15. Fully loaded cost: ₹60–85 per litre.

Branded products retail at ₹250–400 per litre. The difference is margin, marketing, and distribution - not product quality (above a minimum formulation threshold, cleaning performance differences between brands are marginal; consumer testing consistently shows people cannot reliably distinguish between brands in blind trials).

This creates a structural opening for private-label. A retailer with control over formulation standards, contract manufacturing relationships, and direct-to-shelf distribution can offer liquid detergent at ₹149–199/litre - a 50% discount to national brands - while maintaining margins that exceed branded products.

The key is formulation credibility. The private-label liquid must:

1. Match branded performance on the primary cleaning metrics (oil removal, protein removal, whiteness retention)

2. Smell right - fragrance is the single strongest driver of consumer quality perception in detergent, despite having zero cleaning function

3. Pour and dose predictably - viscosity must be calibrated so the product feels "substantial" (not watery) but flows cleanly from the bottle

4. Not damage fabrics - pH must be controlled (7.5–9.5 for liquid, well below powder's 10–11)

A private-label liquid priced at ₹149/litre - offering ₹3.7/wash economics, machine-compatible performance, and adequate fragrance - competes not with branded liquids but with branded premium powders. It pulls consumers forward into the liquid format at a price point that feels like a lateral move, not an upgrade.

This is the wedge. Not competing at the top of the liquid market, but expanding its base.

The Fragrance Paradox

A footnote on something that frustrates every formulation chemist: fragrance is the single most expensive raw material in liquid detergent (after surfactants), contributes nothing to cleaning, and is the primary driver of repeat purchase.

Consumers evaluate detergent quality primarily through post-wash fragrance. Not cleaning efficacy (difficult to assess without controlled comparison), not fabric care (visible only over months), not dissolution quality (invisible). Smell.

This creates a bizarre incentive in formulation: it's rational to invest more in fragrance systems - parfum encapsulation technology that releases scent gradually over hours - than in surfactant optimization that actually cleans better. Brands know this. They spend more R&D money on fragrance stability and "scent boosters" than on cleaning chemistry.

It also means that private-label products, which often invest less in fragrance development, face a perception penalty disproportionate to any actual cleaning gap. The solution isn't to out-invest brands on fragrance (expensive, diminishing returns) but to reach a "good enough" threshold where fragrance doesn't actively detract. In our experience, this threshold is approximately ₹8–12 of fragrance cost per litre of finished product - roughly half of what premium brands spend, but sufficient to avoid the "generic smell" perception that kills repeat purchase.

The Forecast That Matters

Forget the market sizing exercises. Here's the structural prediction:

By 2030, liquid detergent will account for 25–30% of India's fabric care market by value - up from ~10% today. This isn't a forecast; it's a near-mechanical consequence of three forces:

-

Washing machine penetration will rise from ~20% to ~35% of all households (conservative estimate). Every new machine sale is a liquid detergent customer acquisition event.

-

Front-loader share within machines will rise from ~15% to ~30%. Front-loaders functionally require liquid detergent.

-

Urban premiumization continues. Middle-class households that switched from bar to powder in the 2010s will switch from powder to liquid in the 2020s, following the same convenience-and-quality arc.

The bar segment will shrink from ~38% to ~25% of value. Powders will decline from ~50% to ~45%. And liquids will absorb the difference.

For any retailer, the question isn't whether to expand liquid detergent assortment. It's whether to do it now - while consumers are migrating and shelf-share is still negotiable with brands - or later, when the category structure has already locked in and negotiating leverage has shifted.

The Inconvenient Chemistry

We began with a simple experiment: two shirts, two formats, one observable difference.

But the deeper insight isn't about whiteness. It's about information asymmetry. Consumers choose detergents based on pack price, brand familiarity, and fragrance - none of which correlate strongly with cleaning performance. The actual determinants of clean laundry - surfactant dissolution, enzyme activity at wash temperature, builder effectiveness against local water hardness, pH-appropriate fabric care - are invisible to the consumer at point of purchase.

Bridging this gap - through education, through format innovation, through private-label products like Vow that make the better chemistry accessible at the right price point - isn't just a commercial opportunity. It's genuinely useful.

Because every household deserves to understand why their clothes are greying. And the answer, it turns out, isn't "buy more expensive detergent." It's "buy the right format for your water, your machine, and your wash temperature."

Everything else is marketing.

More Retail's fabric care range is available at all More Supermarkets and online on more app.